What Is An IVA?

An IVA can be a great, positive way to help with your debt. Allowing you to continue living your life without the stress of being chased by your creditors. Click to find out more about what an IVA is.

Is An IVA Right For You?

Whether an IVA (Individual Voluntary Arrangement) is right for you or not will largely depend on your personal situation e.g. debt level, number of creditors, affordability etc. Click to find out more.

How Does An IVA Work?

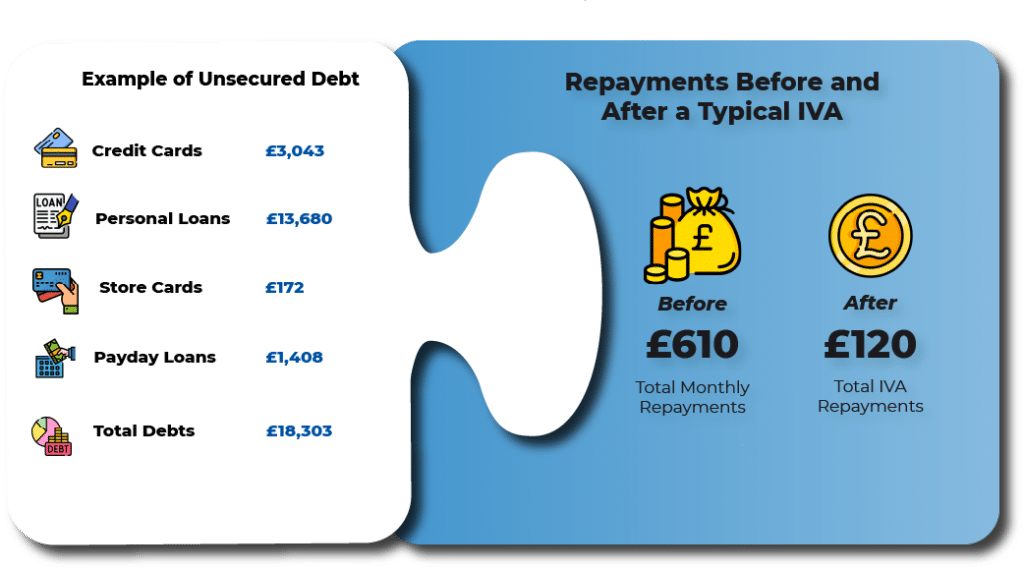

An Individual Voluntary Arrangement (IVA) is a debt solution where you agree with your creditors to pay all or part of your debts. When it is completed, any remaining debts are written off. Take a look at our article to find out more.

Which Debts Can Be Included In An IVA?

Many kinds of debts can be included in an IVA. IVAs are limited to unsecured debts but by solving your unsecured debt problems, you may find paying any secured debt much easier.

How Do I Apply For An IVA?

Applying for an IVA (Indivudual Voluntary Arranagement) is a fairly straightforward process. Click the button below and a member of our team will contact you and guide you through the process.

What Are The Pros & Cons Of An IVA?

As with many things in life, there are benefits and consequences we need to consider. Take a look at our Pros and Cons article to find out whether an IVA is right for you

Does An IVA Have Fees?

Setting up an IVA does incur some costs; however, you will not be expected to pay anything up front at the beginning of the arrangement and there will be no surprise costs at the end of the arrangement.

Logbook Loan Debt

A logbook loan involves borrowing a sum of money secured against your car. By signing up to a logbook loan, you are essentially passing the ownership of your car to the lender in exchange for money. However, you are still allowed to use the car.

Mortgage & Rent Debt

Most people who own their own home, do so with a mortgage. This is a long-term loan, often over the course of 25-30 years, which allows people to borrow sums large enough to cover most of the costs of buying a house.

Secured Loan Debt

When lending money to consumers, some companies like to have the security of attaching the loan to your assets. This gives them the peace of mind that, if something went wrong, they would be able to recover some or all the money through the sale of your property.

Hire Purchase Debt

Hire Purchase (HP) is a type of finance agreement that is often used to purchase motor vehicles or household goods e.g. white goods and furniture. When purchasing vehicles or goods through an HP agreement, you won’t actually own the goods until the last payment has been made and the debt has been cleared.

Council Tax Debt

Council Tax is a yearly fee paid to your local authority, used to pay for all the public services that are in your local area. These include refuse collection, police and fire services, leisure facilities, educational facilities etc. Council tax can either be paid in twelve or ten monthly instalments: the latter giving you two months of payment holiday.

Credit Card Debt

A credit card is a convenient way to borrow money from a bank or lender via the use of a plastic card. You can make purchases in much the same way as when using a debit card. This spending accrues a debt which will have to be paid back at a later date.

Gambling Debt

In simple terms, gambling debt is when a person owes money to a bookmaker or casino. However, things can often become more serious than that, where an individual uses other means of credit to cover their gambling losses.

HMRC Debt

HMRC arrears is any debt amount that relates to Income Tax, National Insurance, VAT or Tax Credit Overpayments. These are ‘High-Priority’ debts and since the consequences can be severe, should be dealt with as soon as possible.

Overdraft Debt

An overdraft is an agreed amount of credit attached to a bank account. It allows your account to fall into a negative balance, where you have spent more than you had in the account. Provided you stay within the agreed limit, this facility should always be available. However, the bank does have the right to withdraw it at any time.

Payday Loan Debt

A Payday Loan allows you to borrow a small amount of money and pay it back once you have received your next wage. This helps you to cover a shortfall in money that may have occurred due to an emergency. They usually carry a high interest rate but can be applied for very quickly in comparison to other types of credit.

Personal Loan

A personal loan is when you borrow an amount of money from a bank, building society or other creditor, agreeing to pay it back over a set repayment term. You will be expected to make equal monthly repayments.

Student Loan Debt

With ever increasing tuition fees, rental prices and living costs, going to university is more expensive than ever. Due to these prohibitive costs, it is incredibly typical for a person to take out student loans and they should, by no means, be considered a bad thing. Unfortunately, for many, they are simply the price of a good education.

Catalogue Debt

Catalogues remain an extremely popular way of purchasing goods for many people, especially around those times of year when money can be short e.g. Christmas and Birthdays.

Store Card Debt

Credit through store cards works in a very similar way to a credit card, however it only authorises you to purchase goods from the store that issued the card. This facility allows you to buy now and pay later or to pay for your goods in instalments if you choose to.

Utility Bills Debt

Few things in life are more essential than your utilities and it’s not an overstatement to say that water, electricity and gas are three things few people can live without. Whether that’s for hydration and sanitation, heating or cooking, or even access to the internet and television, having any of these utilities taken away is unthinkable.

Are IVAs Worth It?

When looking into how an IVA works, there are some features that do appear to be too good to be true, so it is understandable that some people are extremely cautious and even cynical when thinking about whether to proceed.

Is an IVA a Bad Idea?

Whether an IVA is a good or bad idea is largely dependent on your financial circumstances. Of course, every debt solution is going to have its advantages and disadvantages. These need to be considered and weighed up so that you can make an informed choice.

Do You Lose Assets With An IVA?

Assets are the things you own, whether that’s a house, car or electronic equipment. Many people, when entering any debt solution, are often concerned about how much they will lose and to which extent their lives will be altered. Read on to find out more about how an IVA might impact on your assets.