What Is An (Individual Voluntary Arrangement)?

An IVA can be a great, positive way to help with your debt. Allowing you to continue living your life without the stress of being chased by your creditors. Click to find out more about what an IVA is.

Is An Individual Voluntary Arrangement Right For You?

Whether an IVA (Individual Voluntary Arrangement) is right for you or not will largely depend on your personal situation e.g. debt level, number of creditors, affordability etc. Click to find out more.

How Does An Individual Voluntary Arrangement Work?

An Individual Voluntary Arrangement (IVA) is a debt solution where you agree with your creditors to pay all or part of your debts. When it is completed, any remaining debts are written off. Take a look at our article to find out more.

Which Debts Can Be Included In An Individual Voluntary Arrangement?

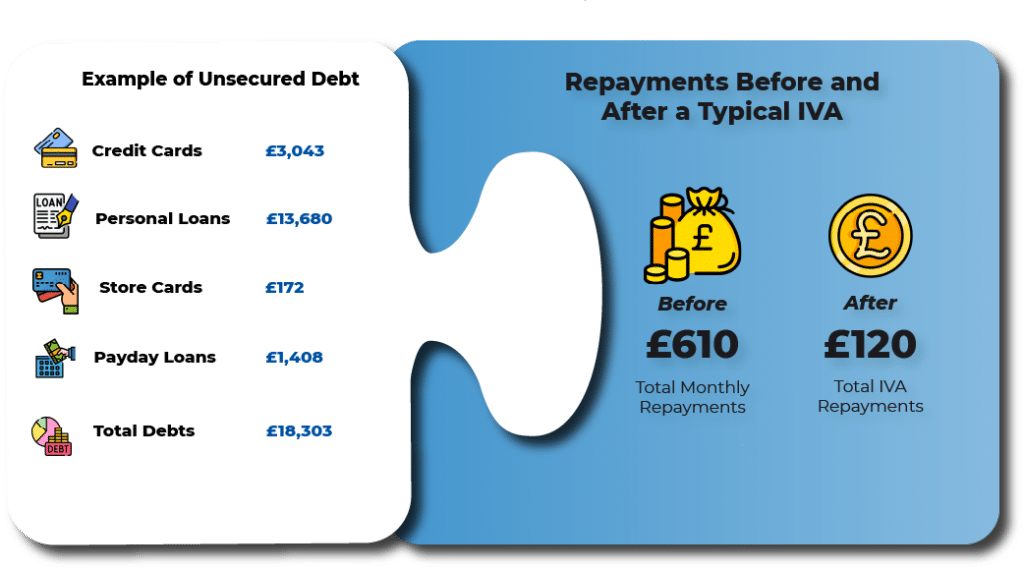

Many kinds of debts can be included in an IVA. IVAs are limited to unsecured debts but by solving your unsecured debt problems, you may find paying any secured debt much easier.

How Do I Apply For An Individual Voluntary Arrangement?

Applying for an IVA (Indivudual Voluntary Arranagement) is a fairly straightforward process. Click the button below and a member of our team will contact you and guide you through the process.

What Are The Pros & Cons Of An Individual Voluntary Arrangement?

As with many things in life, there are benefits and consequences we need to consider. Take a look at our Pros and Cons article to find out whether an IVA is right for you

Does An Individual Voluntary Arrangement Have Fees?

Setting up an IVA does incur some costs; however, you will not be expected to pay anything up front at the beginning of the arrangement and there will be no surprise costs at the end of the arrangement.

Administration Order

For people who have one or more county court judgement made against them, an administration order is a legally binding debt solution which allows you to pay your debt back based on what you can afford.

Bankruptcy

Bankruptcy is a legally binding debt solution. It is often seen as a last resort if other debt solutions fail or can’t be completed within a reasonable timeframe. It is a process whereby debt is written off.

Debt Consolidation Loan

A debt consolidation loan can be an effective way of paying off debt to multiple creditors and combining it into one affordable payment. This allows you to reduce your monthly amount at the cost of more interest.

Debt Management Plan

A Debt Management Plan is an agreement between you and your creditors to reduce your monthly payments. It isn’t a legally binding agreement but can be negotiated by you or a third party on your behalf.

Debt Relief Order

Designed for individuals with very little disposable income, the Debt Relief Order can be accessed if you don’t own your own home and have a debt of no more than £30,000. It is used as an alternative to an IVA.

Debt Settlement Offer

If you acquire a lump sum of money and you have troublesome debts, then a Debt Settlement Offer can enable you to pay that debt at a reduced amount. The repayment is negotiated between you and your creditors.